Portfolio review Jan - June 2020

Half way through 2020, it's been a hectic year in the markets, so lets see how the portfolio got on. My goals haven't changed:

- Don't lose money

- Increase capital by more than the rate of inflation

- Build a conservative dividend paying portfolio

Through doing the above, I will hopefully also outperform the FTSE All

Share Index. I have chosen the FTSE All Share as a benchmark as it most closely

matches the pool of companies from which I’m investing. If I start picking stocks from elsewhere, then I might have to change, but it's good enough for now. I'll take a quick look at each of my stated goals to see how things are looking so far this year for the whole portfolio then pull out a couple of points of interest to see which investments were moving the dials.

Don't lose money

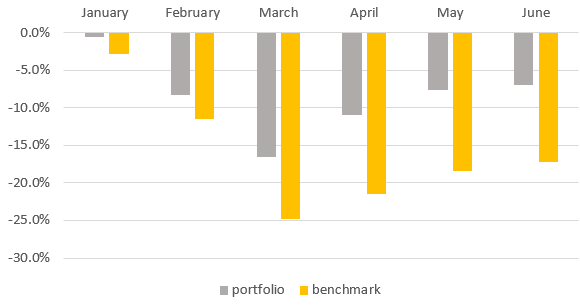

The portfolio remains in the green, as do profits, but it hasn't been a comfortable ride in the first half of the year. Excluding new cash invested, you can see below how both the portfolio measured up against my benchmark from January to June.

The portfolio at the half year mark was roughly 6% below where it was in January, compared to a drop of 17% for the benchmark. It might seem strange to hear that I'm quite pleased by losing 6% over the course of 6 months, but I'm trying to build a resilient portfolio, and by comparison to my benchmark I've not done too badly. My investments fell far less than the wider market, but as that elastic has become stretched, the market is bouncing back quicker than my portfolio. I'm quite content with my investments being less volatile that the market as recovering from large falls in value may take longer than expected.

Increase capital by more than the rate of inflation

On a 6 month timescale this clearly didn't happen, the Office For National Statistics latest inflation stats show it as 0.7%, versus a 6% portfolio fall, so we'll have to see if I can claw that back in the second half of the year. We might well end up with some deflation, if so I could sneak through on a technicality... Essentially this goal is to make sure I'm gaining in real terms, accounting for inflation, so a 6 month timescale is too short a measure to be useful

Build a conservative dividend paying portfolio

Over the past few years big blue chip stocks in the FTSE have provided limited capital growth, instead returning excess cash to investors as dividends. This came to an abrupt halt in 2020 as most companies looked to preserve cash to get them through the various lockdowns happening across the planet. My 15 core portfolio holdings were not immune to this, with 4 of them not paying a dividend in the first half of the year. The language used to describe the lack of dividends varied across the businesses concerned, so we'll have to wait and see if the businesses needed this cash, if they can sensibly invest it or it gets paid out in dividends at a later date.

My preferred measure of the portfolio dividend yield is a rolling 12 month average yield, this has dropped back a bit since the start of the year, from 2.8% to 2.4%, which reflects both a slight reduction in dividend payments, and increased value of the portfolio. My investments are (mostly) in sensibly run, and conservative businesses that I expect to continue to pay out dividends once the current disruption is behind us. Given the axe taken to dividends over this year, I'll consider my dividend receipts a win so far.

Reflections on volatility

I was a little surprised that I was relatively sanguine during the worst of the market collapse. I admit I thought we were going to see the market drop by around 50%, so it faired better than I expected. When it looked like COVID-19 had moved beyond China, I paused my stock buying - in February it looked like the markets were in trouble. This proved to be a good move. I also didn't buy during the March collapse as I was trying to work out which businesses on my shopping list would be hit hard by the virus and/or lockdown measures, and which might be resilient. Not buying in March proved to be incorrect. Although I didn't suffer an immediate loss in Feb, I would have benefited from buying as the markets bottomed in March.

Porfolio winners and losers

One of my core holdings, Compass, has been hit hard by the lockdowns. It provides catering services and since most events and companies have been either closed or happening virtually, demand for catering took a big hit. Trading updates indicated that around 50% of the business was closed. I'm comfortable staying invested, with the assumption that their scale will be a benefit over the long term.

The contribution that each of the portfolio has made to the first half results is below:

Compass is the clear outlier dragging down performance significantly. This is partly due to the fall in share price, but also to it being my 4th largest holding at the start of the year.

Individual performance of investments is below:

The two members of the portfolio I was thinking of selling 6 months ago, I dithered over. As a result Saga and Dignity are still there, albeit very small holdings. I'm in two minds whether to get rid of them, as they are irritants, and I don't regard either as sensible investments. Saga may see a decent bounce if we get good news on the medical front that enables it's cruise ships to set off. One the other hand, they are both very small amounts of cash, so unlikely to have much impact on the overall portfolio whichever way they move.

There are plenty of reasons to be concerned over the state of the markets, with an imminent global recession, US attempts to address the virus seemingly unravelling, a US election, Trumpy's fondness for tariffs, and Brexit. However I suspect all will be ignored if we get good news on vaccines and medical treatments for the virus. Whether that good news is already priced in we will find out in due course...